How Investment Banks Actually Make Money: From a student Lens

Rawwaf Altuwirji - MALTECH

Why this matters

If you're applying to banks or just curious about how they work, understanding how investment banks actually make money is non-negotiable. It’s not just about “Wall Street greed” — IBs operate in complex, layered ways. As students, we often hear names like “Goldman Sachs” or “J.P. Morgan” without knowing what they actually do to generate revenue.

|

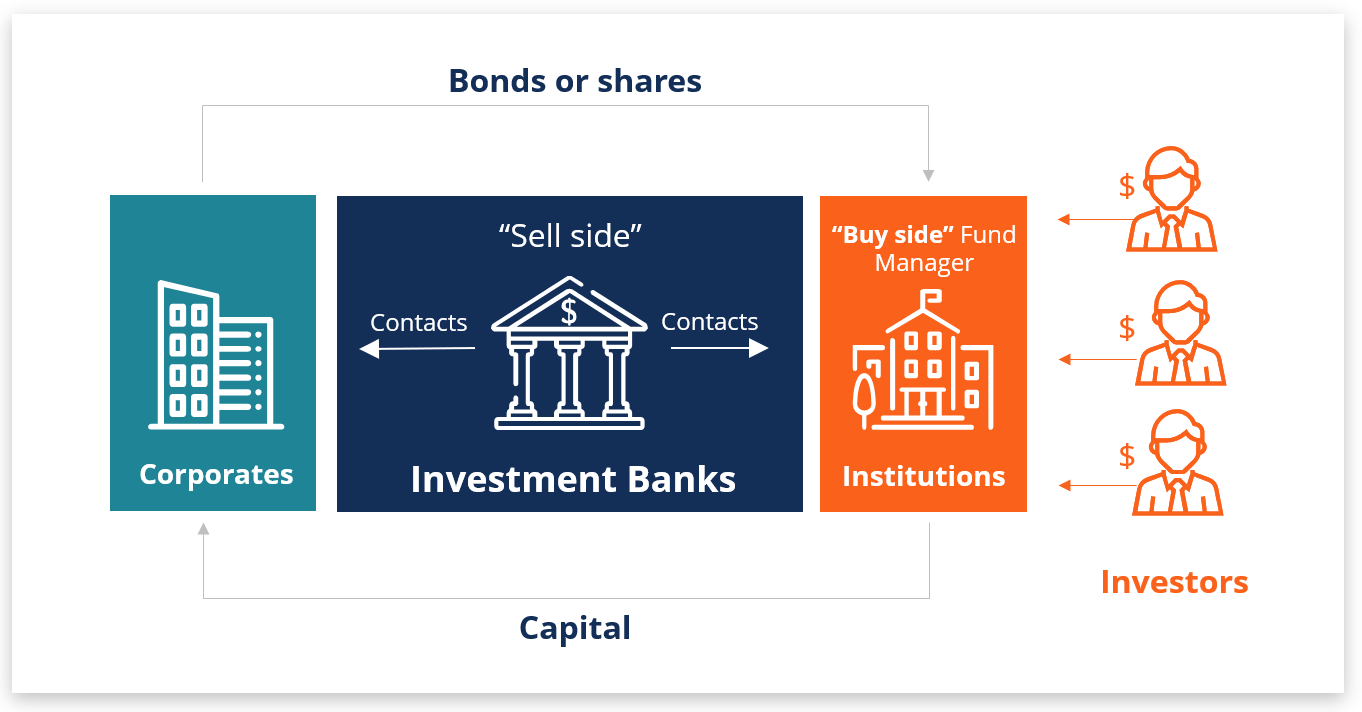

| CFI |

The 3 Main Revenue Streams

1. Advisory Fees (Investment Banking Division – IBD)

This is what most people think of when they hear “investment bank” — big firms advising on mergers, acquisitions (M&A), and IPOs.

Example: When a company wants to go public or buy another company, banks provide strategic advice and help with the deal structure.

Revenue Source: Banks charge a percentage of the deal size — usually 0.5% to 2%, depending on the complexity and size.

Student angle: These deals are huge — a $1 billion acquisition could generate $10–20 million in fees.

2. Underwriting (Capital Markets Divisions: ECM & DCM)

Here, banks help companies raise capital by issuing new stocks (ECM – Equity Capital Markets) or bonds (DCM – Debt Capital Markets).

Example: A startup becomes big and wants to raise £200 million by selling shares — the bank handles the whole process.

Revenue Source: Banks buy the securities at a discount, then sell them to investors for a profit (called the “spread”).

Student insight: You’ll hear “bookrunner” or “lead manager” on LinkedIn job descriptions — this is where it fits in.

3. Trading & Asset Management (Markets Division)

This is the more technical side — sales and trading (S&T), market-making, and managing client portfolios.

Revenue Sources:

Bid-ask spreads from trading

Management fees from handling institutional or high-net-worth money

Proprietary trading (banks trading for their own profit — limited after 2008 due to regulation)

Note: A lot of the shift toward quant roles is happening here — algorithms now handle large volumes of trades.

Do All Investment Banks Do All These Things?

No.

Bulge Brackets (e.g., Goldman Sachs, Morgan Stanley): Do it all — global scale, multiple divisions.

Boutiques (e.g., Evercore, Lazard): Mostly focus on M&A and advisory.

Commercial Banks with IB arms (e.g., HSBC, Barclays): Mix of traditional banking and IB services.

Final Thoughts

Investment banks generate revenue by positioning themselves at the center of the financial system. Whether advising on a merger, raising capital, or facilitating global markets, they extract value by providing access, expertise, and liquidity.

Their business model is built around transactions, relationships, and market flows—each division playing a distinct but interconnected role. Understanding these revenue streams is essential for anyone seeking clarity on how the industry functions at its core.

References:

https://corporatefinanceinstitute.com/resources/career/investment-banking-overview/

https://www.investopedia.com/terms/i/investment-banking.asp

https://www.cfainstitute.org/programs/cfa-program/careers/investment-banker

Comments

Post a Comment